Bottom Line: A 720 credit score is achievable 12–24 months after bankruptcy discharge. At Sacks & Sacks, every bankruptcy client receives our 7 Steps to a 720 Credit Score program — a $1,000 value — at no cost. Call (904) 396-5557 for a free consultation.

Melanie Sacks — Jacksonville bankruptcy attorney, FL Bar #158070, 27+ years of experience, 6,354+ cases filed. Martindale-Hubbell BV Distinguished.

Can You Really Reach a 720 Credit Score After Bankruptcy?

Yes — and the data backs it up. FICO defines a “good” credit score as 670–739, and a 720 puts you squarely in that range (Experian). The average American’s FICO score is 715 as of 2025 (CNBC/FICO), meaning a 720 after bankruptcy would put you above the national average. Research from Dworken & Bernstein shows that nearly two-thirds of filers reach 640 or higher within two years. With structured credit rebuilding through a program like our 7 Steps to a 720, reaching that target in 12–24 months is realistic for most Jacksonville bankruptcy clients.

Research from Dworken & Bernstein found that nearly two-thirds of bankruptcy filers reach a credit score of 640 or higher within two years of discharge — and the average score five years after bankruptcy reaches 672. With structured credit rebuilding, hitting 720 in 12–24 months is realistic.

At the Law Offices of Sacks & Sacks, P.A., we have helped Jacksonville families rebuild their financial lives for decades. Our 7 Steps to a 720 Credit Score program gives every bankruptcy client a proven, step-by-step roadmap — included free with your case.

Why Jacksonville Residents Are Filing for Bankruptcy

Florida saw 40,679 bankruptcy filings in the 12-month period ending June 2025, up from 32,933 the year before — a 23.5% increase (Florida Trend). The Middle District of Florida, which includes Jacksonville, is the third-busiest bankruptcy court out of all 90 federal districts nationwide. Jacksonville’s division alone recorded 4,007 filings in 2024, a 21% increase from the prior year (FLMB, 2024). Rising costs of living, medical debt, credit card delinquency rates climbing to 14.1%, and post-pandemic financial strain are driving these numbers higher across the state. For many of these filers, the decision to file bankruptcy is the first step toward rebuilding their credit and their financial future.

Nationally, 529,080 bankruptcy cases were filed in the 12-month period ending March 2025 — a 13.1% jump over the previous year (U.S. Courts). Rising costs of living, medical debt, and post-pandemic financial strain are driving these numbers higher.

If you are considering bankruptcy in Jacksonville, know this: filing is not the end. It is the beginning of a financial fresh start — and rebuilding your credit is the first step.

Every Sacks & Sacks Bankruptcy Client Gets Our 720 Credit Score Program FREE

A $1,000 credit education program — included at no cost with your bankruptcy case.

The 7 Steps to a 720 Credit Score After Bankruptcy

Step 1: Dispute Credit Report Errors Immediately

Your first move after discharge is to pull your credit reports from all three bureaus — Equifax, Experian, and TransUnion — through AnnualCreditReport.com (free). Errors on credit reports are common: according to the FTC, one in five consumers has a verified error on at least one credit report.

After bankruptcy, you want to confirm that:

- All discharged debts show a $0 balance

- No discharged accounts are listed as “open” or “past due”

- The same debt is not listed twice under different creditor names

- Your bankruptcy discharge date is accurately recorded

If you find errors, dispute them in writing with each credit bureau. Under the Fair Credit Reporting Act (FCRA), bureaus must investigate within 30 days and either correct or verify the entry. Removing inaccurate negative marks can boost your score immediately.

Step 2: Open the Right Credit Cards

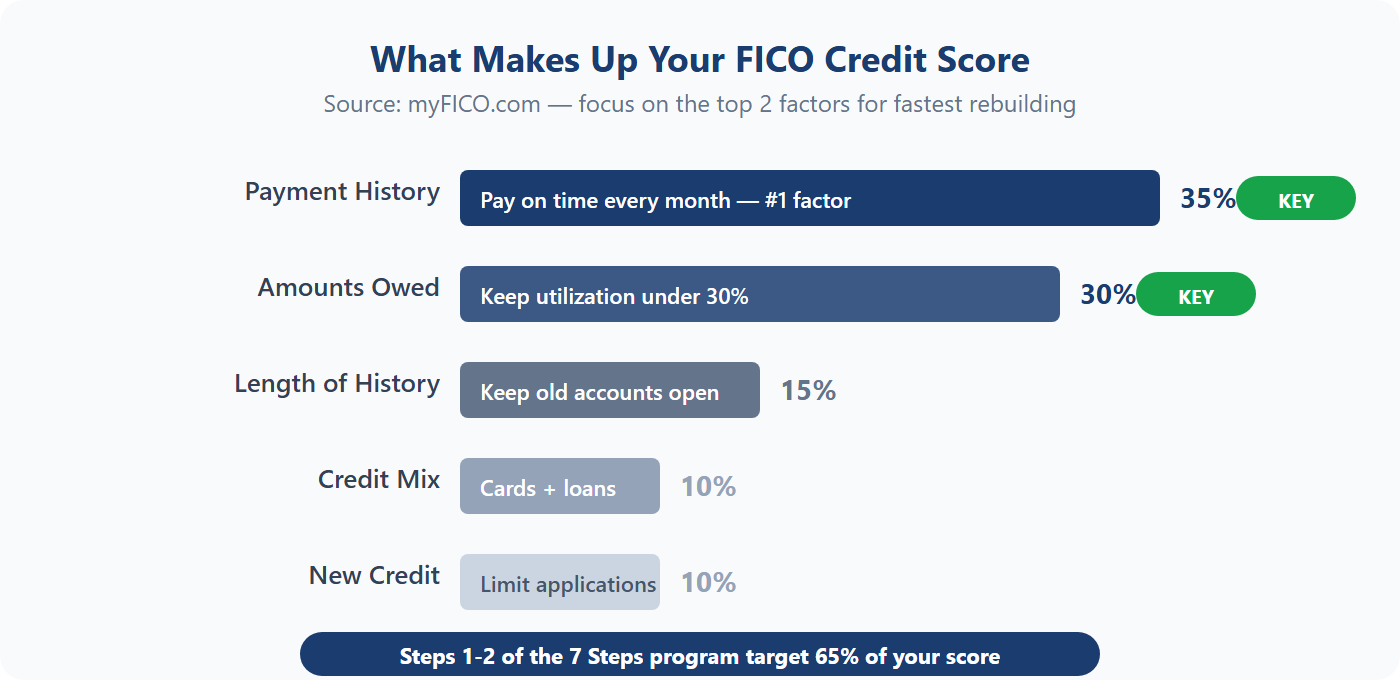

Credit card usage accounts for a significant portion of your FICO score — amounts owed make up 30% of the calculation (myFICO). The key is using credit cards strategically:

- Start with a secured credit card. You deposit $200–$500 as collateral. Your spending limit equals your deposit, so the risk is low. Make small purchases (under 30% of your limit) and pay the full balance monthly.

- Graduate to an unsecured card after 6–12 months of on-time payments. Many secured card issuers will upgrade you automatically.

- Keep utilization below 30%. If your limit is $500, keep your balance under $150 at all times. Lower utilization signals responsible credit use to scoring models.

Paying your credit cards on time every month is the single most important factor — payment history makes up 35% of your FICO score (Bankrate).

Step 3: Add an Installment Loan to Your Credit Mix

FICO rewards a healthy mix of credit types — revolving (credit cards) and installment (loans with fixed monthly payments). Credit mix accounts for 10% of your score (myFICO).

A credit-builder loan is designed specifically for this purpose. Unlike a traditional loan, the lender holds the funds in a restricted account while you make monthly payments. Once paid off, you receive the money — and you have built a track record of on-time installment payments.

Credit unions in Jacksonville often offer credit-builder loans with low fees. Typical amounts are $500–$1,500 with 12–24 month terms. Every on-time payment is reported to the credit bureaus, steadily raising your score.

Step 4: Use Quick Credit Strategies for an Early Boost

Several tactics can accelerate your credit rebuilding in the first few months after discharge:

- Become an authorized user. Ask a trusted family member with a long, clean credit history to add you as an authorized user on their credit card. Their positive payment history gets reported on your credit report, too. You do not even need to use the card — just having your name on the account helps.

- Get a co-signer for a small loan. A co-signer with good credit improves your approval odds and may qualify you for a lower interest rate. A small auto loan or personal loan with on-time payments builds your credit file.

- Report rent and utility payments. Services like Experian Boost and similar platforms let you add rent, utility, and streaming payments to your credit report — giving you credit for bills you already pay on time.

Step 5: Monitor Your Credit Reports and Scores Monthly

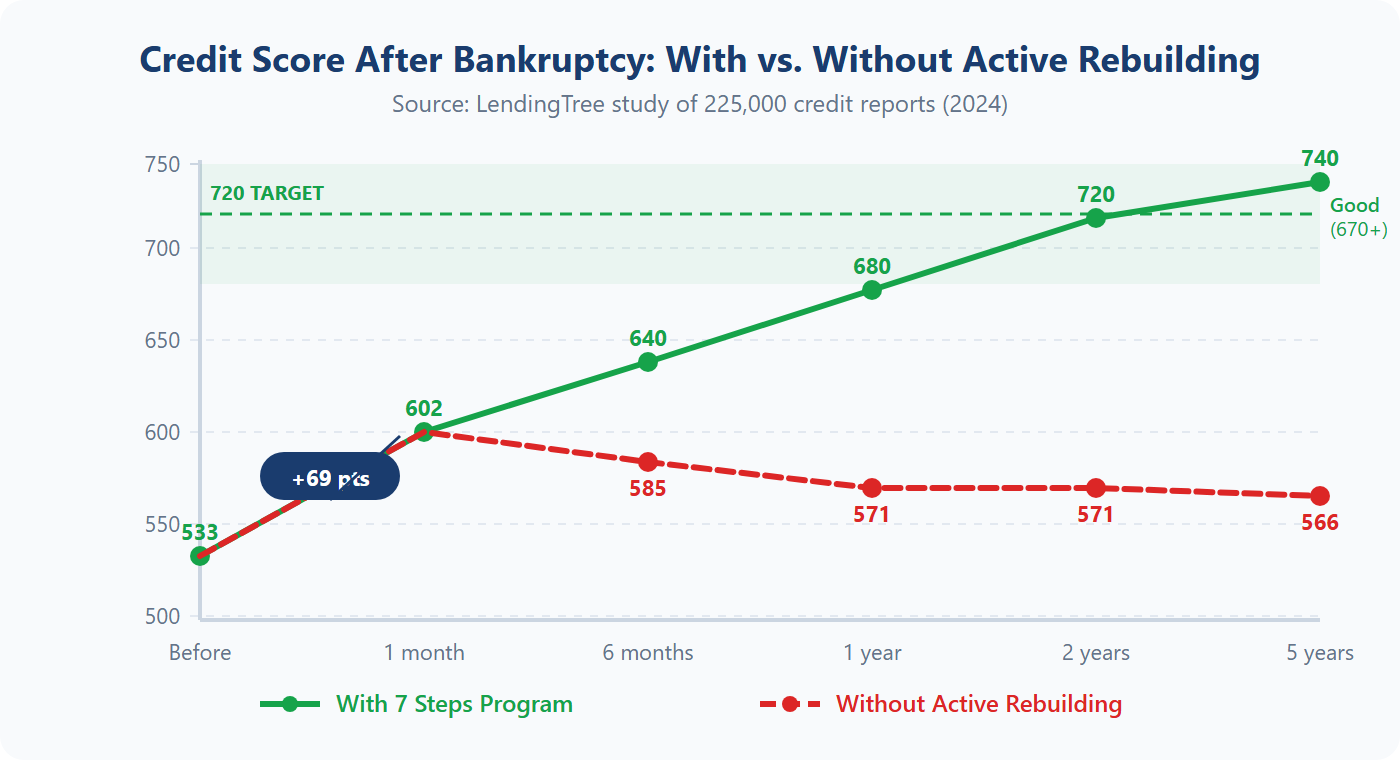

Rebuilding credit is a process, and tracking your progress keeps you on course. The LendingTree study found that without active monitoring, consumers’ average scores dropped from 602 one month after filing to 571 within one to two years — and all the way to 566 after five years (LendingTree, 2024).

That backslide is preventable. Here is what to monitor:

- Credit score changes — free through your bank, credit card issuer, or Credit Karma

- New inquiries — each hard inquiry can temporarily lower your score by 5–10 points

- Utilization ratio — aim to stay under 30%, and ideally under 10%

- Payment history accuracy — ensure every on-time payment is correctly reported

A 720 credit score is classified as “good” by FICO (670–739) and “prime” by VantageScore. At this level, you qualify for competitive interest rates on mortgages, auto loans, and credit cards — saving thousands of dollars over the life of a loan.

Step 6: Pay Down Your Highest-Interest Debt First

If you have any remaining balances after bankruptcy — such as non-dischargeable debts like student loans or tax obligations — prioritize paying down the highest-interest balance first. This is known as the avalanche method, and it saves the most money over time.

For credit card balances specifically:

- Pay more than the minimum every month

- Target the card with the highest APR first while making minimum payments on others

- Once the highest-interest card is paid off, roll that payment into the next card

Reducing your overall credit utilization from high (50%+) to low (under 30%) can produce a noticeable score improvement within one to two billing cycles.

Step 7: Protect Your Credit — and Keep Building

Once you reach a 720 credit score, maintaining it requires consistency. A LendingTree analysis found that more than five years after bankruptcy, the average consumer’s score dropped to 566 — with average credit card balances climbing to $5,908 and utilization hitting 49.9%. The consumers who avoided this pattern were those who maintained disciplined habits.

To protect your rebuilt credit:

- Never miss a payment. Set up autopay for at least the minimum due on every account.

- Keep old accounts open. Length of credit history accounts for 15% of your FICO score. Even if you do not use a card, keeping it open helps.

- Limit new credit applications. Only apply for credit you need. Each application triggers a hard inquiry.

- Review your reports annually. Errors can reappear. Stay vigilant.

What Happens to Your Credit Score During Bankruptcy?

Filing for bankruptcy typically drops your credit score by up to 200 points (Experian), but that figure is misleading because most people considering bankruptcy already have severely damaged credit from missed payments, collections, and high utilization. The LendingTree study of 225,000 credit reports revealed a surprising pattern: the average filer’s score actually increased 69 points — from 533 to 602 — within the first month after filing. Average credit card balances dropped 87.5% (from $7,571 to $950), and utilization ratios fell from 53.1% to 14.9%. The slate is wiped clean, and that is the foundation that makes reaching a 720 credit score possible within 12–24 months with structured rebuilding through the Sacks & Sacks program.

Why? Because bankruptcy eliminates the debt dragging your score down. Average credit card balances dropped 87.5% (from $7,571 to $950), and utilization ratios fell from 53.1% to 14.9%. The slate is wiped clean — and that is the fresh start that makes reaching 720 possible.

The timeline depends on which chapter you file:

- Chapter 7 bankruptcy stays on your credit report for 10 years but can be discharged in as little as 3–6 months. Most of our Jacksonville clients begin seeing meaningful credit improvement within 6–12 months.

- Chapter 13 bankruptcy stays on your credit report for 7 years and involves a 3–5 year repayment plan. Credit rebuilding begins during the plan as you demonstrate consistent payment history.

Why I Include the 720 Credit Score Program Free

Most credit rebuilding programs charge around $1,000 for enrollment, and many lack the legal context needed to help bankruptcy filers specifically. I developed the 7 Steps to a 720 Credit Score program after 27+ years of practice (FL Bar #158070) and more than 6,354 cases filed in Jacksonville because I saw too many clients walk out of my office with a discharge order and no plan for what comes next. The LendingTree study found that without active rebuilding, the average filer’s score drops from 602 one month after filing to just 566 after five years. That backslide is entirely preventable. Getting out of debt is only half the journey — rebuilding your financial life is the other half, and most attorneys ignore it entirely.

Every bankruptcy client at Sacks & Sacks receives the 7 Steps to a 720 Credit Score program at no additional cost. The program includes step-by-step credit education, ongoing guidance, and a proven framework that has helped clients across Jacksonville rebuild their credit and qualify for mortgages, auto loans, and credit cards within 12–24 months of discharge.

In 27 years and more than 6,354 cases, I’ve watched clients go from financial crisis to buying homes, financing cars, and opening businesses — all because they followed this program. That transformation is why I do this work.

Client Reviews — See What People Are Saying

Ready to Rebuild Your Credit After Bankruptcy?

Call me for a free consultation. I’ll review your situation and tell you exactly what bankruptcy can do for you — and how the 720 Credit Score program will help you rebuild. No judgment, no pressure.

Frequently Asked Questions

How long does it take to get a 720 credit score after bankruptcy?

With consistent effort and the right strategy, most people can reach a 720 credit score within 12–24 months of their bankruptcy discharge. Research shows that nearly two-thirds of bankruptcy filers reach 640 or higher within two years (Dworken & Bernstein). Our 7 Steps program helps clients accelerate this timeline by providing a structured, proven approach to credit rebuilding.

Does filing for bankruptcy destroy your credit forever?

No. While Chapter 7 bankruptcy stays on your credit report for 10 years and Chapter 13 for 7 years, the impact on your score decreases significantly over time. A LendingTree study found that the average filer’s score increased 69 points within the first month of filing (LendingTree, 2024). Many of our clients qualify for competitive mortgage rates within 2–4 years of discharge.

Can I get a mortgage after filing bankruptcy in Florida?

Yes. FHA loans are available as soon as 2 years after a Chapter 7 discharge or 1 year into a Chapter 13 repayment plan. Conventional mortgages typically require a 4-year waiting period after Chapter 7 or 2 years after Chapter 13 discharge. Reaching a 720 credit score before applying will qualify you for the best available interest rates.

What credit score do most people have after filing bankruptcy?

According to the LendingTree study, the average credit score one month after bankruptcy is 602. However, without active credit rebuilding, scores tend to decline — dropping to an average of 571 within one to two years and 566 after five years. Active credit rebuilding through a structured program prevents this backslide and pushes scores higher.

Is the 7 Steps to a 720 Credit Score program really free at Sacks & Sacks?

Yes. The program typically costs $1,000, but every bankruptcy client at the Law Offices of Sacks & Sacks, P.A. receives enrollment at no additional charge. We include it because we believe a true fresh start means more than just debt relief — it means a clear path to rebuilding your financial future.

Should I file Chapter 7 or Chapter 13 bankruptcy in Jacksonville?

It depends on your income, assets, and debts. Chapter 7 (liquidation) eliminates most unsecured debts in 3–6 months and is best for those who pass Florida’s means test. Chapter 13 (reorganization) creates a 3–5 year repayment plan and is often better for homeowners facing foreclosure. Our Jacksonville bankruptcy attorneys can evaluate your situation during a free consultation and recommend the best option.

How many people file for bankruptcy in Florida each year?

Florida had 40,679 bankruptcy filings in the 12-month period ending June 2025, a 23.5% increase over the prior year (Florida Trend). The Middle District of Florida, which includes Jacksonville, is the third-busiest bankruptcy court among all 90 federal districts. You are not alone — and filing is often the smartest financial decision you can make.

Sources

- LendingTree. “Consumers See Immediate Credit Score Improvements (but Long-Term Consequences) After Filing for Bankruptcy.” October 2024. lendingtree.com

- Experian. “What Is a Good Credit Score?” 2025. experian.com

- CNBC/FICO. “What’s The Average Credit Score?” February 2025. cnbc.com

- Dworken & Bernstein. “The Real Impact of Bankruptcy on Credit.” dworkenlaw.com

- U.S. Courts. “Bankruptcies Rise 13.1 Percent Over Previous Year.” May 2025. uscourts.gov

- Florida Trend. “Bankruptcy Filings Jump in Florida.” August 2025. floridatrend.com

- U.S. Bankruptcy Court, Middle District of Florida. “Facts & Statistics.” flmb.uscourts.gov

- Bankrate. “How to Rebuild Your Credit After Filing For Bankruptcy.” June 2025. bankrate.com

- Experian. “How Does Filing Bankruptcy Affect Your Credit?” experian.com

- myFICO. “What’s in Your Credit Score.” myfico.com

- Federal Trade Commission. “Disputing Errors on Credit Reports.” consumer.ftc.gov

Serving Jacksonville, Orange Park, St. Augustine, Fernandina Beach, and all of Northeast Florida. Virtual consultations available — no office visit required.

Related: Jacksonville Bankruptcy Lawyer | Chapter 7 Bankruptcy | Chapter 13 Bankruptcy | Personal Bankruptcy | Business Bankruptcy | Fast File Bankruptcy | Debt Consolidation