Melanie Sacks — Jacksonville bankruptcy attorney, FL Bar #158070, 27+ years of experience, 6,354+ cases filed. Martindale-Hubbell BV Distinguished.

Why Jacksonville Residents Are Rethinking Debt Consolidation

Florida bankruptcy filings reached 37,156 in 2024 — a reflection of the financial strain facing households across the state (Debt.org, 2025). [3] Nationally, bankruptcy filings surged 11.8% in 2025 to over 542,000 cases, driven by $1.21 trillion in outstanding credit card debt and delinquency rates climbing to 14.1%. [2] Meanwhile, debt consolidation programs continue to fail the majority of applicants — a Hoyes Michalos study found that 80% of applicants do not qualify for favorable consolidation terms, and those who enroll face a 32% dropout rate due to unaffordable fees. [1] As a Jacksonville bankruptcy attorney with 22+ years of experience and more than 6,354 cases filed (FL Bar #158070), I help families weigh both options honestly. Many of my clients come to me after spending months or years in consolidation programs that left them deeper in debt.

Many people in Jacksonville explore debt consolidation first, hoping to combine multiple debts into a single monthly payment. In my 27 years of practice, I’ve seen this pattern repeat thousands of times: a client spends a year or more making payments to a consolidation company, only to find their total debt has grown because interest kept compounding while fees piled up.

At The Law Offices of Sacks & Sacks, P.A., I help Jacksonville families understand when debt consolidation makes sense and when bankruptcy provides a faster, more complete path to financial recovery.

What Is Debt Consolidation?

Debt consolidation combines multiple debts — credit cards, medical bills, personal loans, and other unsecured obligations — into a single monthly payment, ideally at a lower interest rate than you are currently paying. For Jacksonville residents carrying an average of $97,147 in total debt, the appeal is straightforward: one payment instead of many, a potentially lower interest rate, and the ability to avoid a bankruptcy filing on your credit report. However, the reality is more complicated than the marketing suggests. Consolidation does not reduce the amount you owe — it only restructures the payment terms — and creditor participation is entirely voluntary, meaning your lenders can refuse to cooperate at any time. There are three primary ways debt consolidation works, and each has significant limitations:

- Debt consolidation loans — A new personal loan used to pay off existing debts

- Debt management plans (DMPs) — A credit counseling agency negotiates reduced interest rates with your creditors

- Balance transfer credit cards — Moving balances to a card with a low introductory rate (typically 12-18 months)

The appeal is straightforward: one payment, potentially lower interest, and no bankruptcy on your credit report. But the reality is more complicated.

5 Problems With Debt Consolidation in Florida

A Hoyes Michalos study found that 80% of debt consolidation loan applicants fail to qualify because the credit scores needed for favorable rates are higher than most struggling borrowers carry. [1] The fundamental problem is this: by the time most Jacksonville residents consider debt consolidation, their credit has already deteriorated to a level that disqualifies them from the very programs being marketed to them. Debt settlement companies typically require credit scores above 670 for favorable terms, yet most people seeking debt relief have scores well below that threshold. For the 20% who do qualify and enroll, a DebtWave 2024 study found that 32% drop out because the combination of enrollment fees, monthly maintenance fees, and settlement fees — often totaling 15-25% of enrolled debt — proves unaffordable. Here are the five most common problems I see with debt consolidation in my Jacksonville practice:

- No guarantee creditors will participate. Debt consolidation is voluntary — your creditors can refuse to negotiate or accept reduced payments. In bankruptcy, creditor participation is mandatory and court-ordered.

- High upfront fees drain your resources. Consolidation companies charge enrollment fees, monthly maintenance fees, and settlement fees that can total 15-25% of your enrolled debt. A DebtWave 2024 study found 32% of enrollees dropped out because fees were unaffordable.

- Interest and late fees keep compounding. While you save money in a consolidation account, your creditors may continue charging interest, late fees, and penalties. Your balance can grow faster than your payments. In bankruptcy, an automatic stay halts all collection activity, interest, and fees the moment you file.

- Forgiven debt triggers tax liability. Under IRS rules, any debt reduced by more than $600 through consolidation or settlement is reported as taxable income on a 1099-C. Debt discharged through bankruptcy creates no tax burden.

- Your credit score takes a hit anyway. Missed payments during consolidation negotiations, closed accounts, and settlement notations damage your credit — often as severely as bankruptcy, but without the clean slate that follows discharge.

Debt Consolidation vs. Bankruptcy: Side-by-Side Comparison

| Factor | Debt Consolidation | Chapter 7 Bankruptcy | Chapter 13 Bankruptcy |

|---|---|---|---|

| Timeline | 3-5 years | 3-4 months to discharge | 3-5 year repayment plan |

| Debt eliminated | None — you repay in full (or negotiated amount) | Most unsecured debt discharged completely | Remaining unsecured debt discharged after plan |

| Creditor cooperation | Voluntary — creditors can refuse | Court-ordered — mandatory | Court-ordered — mandatory |

| Collection calls/lawsuits | May continue | Automatic stay stops all collection | Automatic stay stops all collection |

| Interest/fees | Can continue accruing | Frozen at filing | Frozen at filing |

| Tax consequences | Forgiven debt is taxable income | No tax on discharged debt | No tax on discharged debt |

| Credit recovery | Gradual, with settlement marks | 100-150 point increase within 6-12 months [4] | Steady improvement during repayment plan |

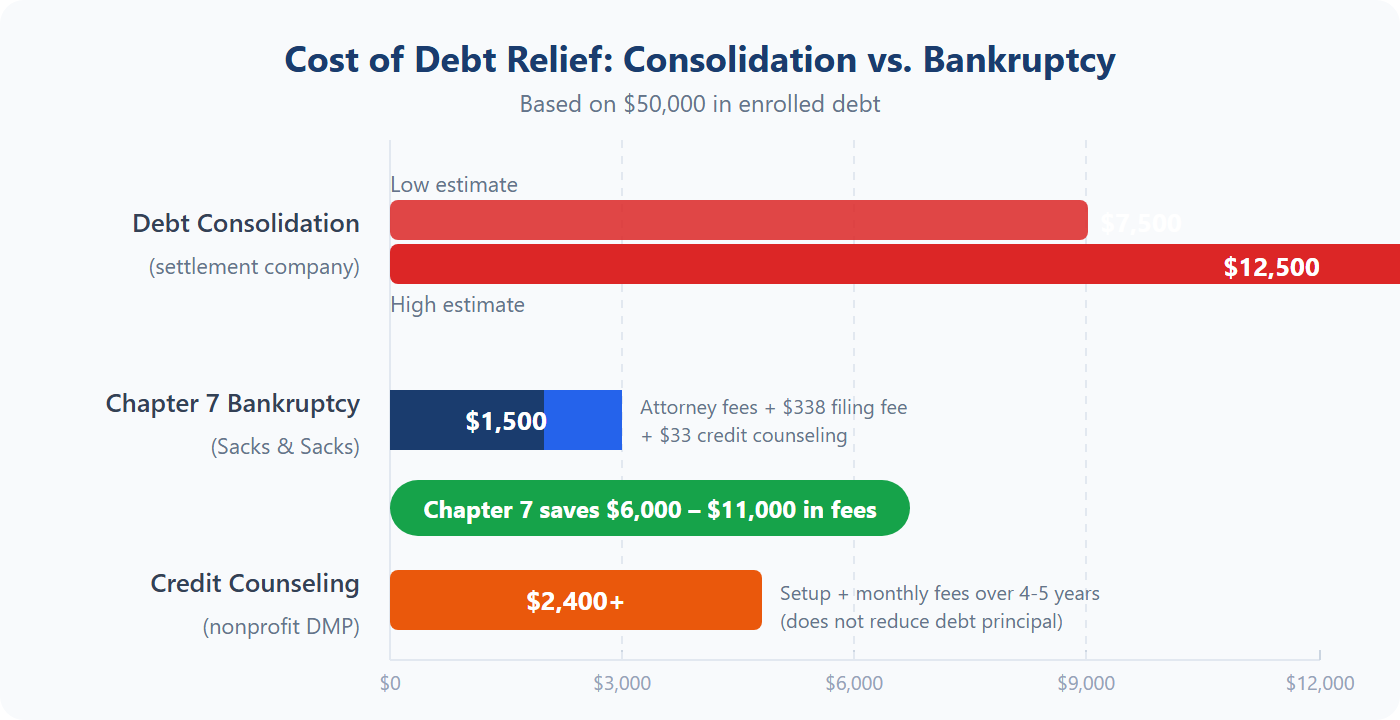

| Cost | 15-25% of enrolled debt in fees | Attorney fees + $338 filing fee | Attorney fees + $313 filing fee |

When Bankruptcy Is the Better Choice

For many Jacksonville residents carrying significant debt, bankruptcy provides faster and more complete relief than consolidation — and the long-term financial outcomes support this. Upsolve tracking data shows that 70% of Chapter 7 filers report improved financial stability within three years of discharge, and half secure new lines of credit within 12-18 months. [5] A 2023 American Personal Finance Study Commission whitepaper found Chapter 7 filers had 25% higher net worth after five years compared to those who pursued consolidation alone. Unlike consolidation, bankruptcy provides court-ordered protection through the automatic stay under 11 U.S.C. § 362, which immediately halts creditor calls, wage garnishments, lawsuits, and interest accrual. Chapter 7 cases in Jacksonville typically complete in 3-4 months, while consolidation programs drag on for 3-5 years with a 32% dropout rate. [1] Bankruptcy is the stronger option if you meet any of these criteria:

Bankruptcy may be the stronger option if you:

- Owe more than you can realistically repay within 3-5 years

- Face wage garnishment, lawsuits, or creditor harassment

- Have a credit score too low to qualify for favorable consolidation terms

- Need immediate protection from collection through an automatic stay

- Want a defined endpoint rather than years of negotiation

Bankruptcy is not failure — it is a legal tool designed to give honest people a genuine fresh start. Most of my clients wish they had filed sooner instead of spending years and thousands of dollars on consolidation programs that never worked.

When Debt Consolidation May Work

Debt consolidation can be effective in specific, limited situations where the borrower’s financial profile supports it. Not everyone needs bankruptcy, and I am upfront about that during every consultation at my Jacksonville office. If your total unsecured debt is manageable — typically under $20,000 — and your credit score is above 670, consolidation may offer a viable path to becoming debt-free without the consequences of a bankruptcy filing. The key distinction is that consolidation works best for people experiencing temporary financial strain rather than a structural inability to repay. In my 22+ years of practice (FL Bar #158070), I have recommended consolidation over bankruptcy when the numbers clearly supported it. Here are the specific conditions where consolidation tends to work:

- Your credit score is above 670, qualifying you for a lower interest rate

- Your total unsecured debt is manageable (typically under $20,000)

- You have steady income to make consistent payments

- You want to avoid a bankruptcy filing on your credit report

If you are considering consolidation, be cautious of companies that charge large upfront fees, guarantee results, or pressure you into signing quickly. A legitimate credit counseling agency approved by the U.S. Department of Justice can review your options at no cost.

How I Help Jacksonville Families Choose the Right Path

I do not push bankruptcy on everyone who walks through my door — and I never have. In 22+ years of practice and more than 6,354 cases filed in Jacksonville’s Middle District of Florida, I have learned that the right solution depends entirely on your specific financial situation. Some clients need the immediate protection of the automatic stay under 11 U.S.C. § 362. Others need guidance on consolidation options, credit counseling, or debt negotiation strategies that do not involve a bankruptcy filing. My job is to evaluate your complete financial picture and give you an honest recommendation, even when that recommendation is not bankruptcy. During your free consultation, I will:

- Review your complete financial picture — income, debts, assets, and monthly expenses

- Compare your options side by side — consolidation, Chapter 7, Chapter 13, or debt negotiation

- Calculate the true cost of each path — including fees, tax implications, and timeline to becoming debt-free

- Give you an honest recommendation — whether that is bankruptcy or an alternative

You don’t even need to leave your house. I handle everything virtually — from the initial consultation to filing your petition. Most clients never step foot in a courtroom.

And every bankruptcy client at Sacks & Sacks receives complimentary enrollment in my 7 Steps to a 720 Credit Score program — because I believe getting out of debt is only half the journey. Rebuilding is the other half, and most attorneys ignore it entirely.

Why Jacksonville Families Trust Sacks & Sacks

I have practiced bankruptcy law in Jacksonville since 1998 — 22+ years representing individuals and families in Duval County and throughout Northeast Florida. In that time, I have filed more than 6,354 bankruptcy cases and helped over 10,000 clients navigate the decision between debt consolidation, Chapter 7 liquidation, and Chapter 13 reorganization. I have seen every situation: medical debt that spiraled after a hospital stay, credit card balances that ballooned during a divorce, income loss from job elimination, and small business failures that left personal guarantees behind. The Middle District of Florida is the third-busiest bankruptcy court in the nation, and I have practiced in this district for my entire career. Whatever brought you here, I have helped someone in your exact position before.

- 6,354+ bankruptcy cases filed in the Jacksonville Division

- 27+ years licensed in Florida — Florida Bar #158070 (since 1998)

- Martindale-Hubbell “BV Distinguished” Rating for exceptional legal ability and high ethical standards

- 4.8 Avvo rating (49 client reviews) • 4.7-star average across 187+ verified reviews

- Three Best Rated® — Top 3 Bankruptcy Lawyers in Jacksonville, FL

- Member: American Bankruptcy Institute, National Association of Consumer Bankruptcy Attorneys, Jacksonville Bankruptcy Bar Association

- J.D.—Thomas M. Cooley Law School (1998) • B.A.—University of Florida (1992)

- Profiled on Martindale-Hubbell • Justia • LinkedIn

“I enthusiastically endorse Melanie Sacks as one of the best Consumer Bankruptcy attorneys that I know! Melanie is superbly skilled and knowledgeable in both Chapter 7 and Chapter 13 practice.”

— Peer Attorney Endorsement

What Our Jacksonville Clients Say

“I was very nervous about declaring bankruptcy but Melanie and her staff were so helpful and considerate that I was immediately put at ease. Everyone there was extremely accessible and we spoke with Melanie several times during the process and she always assured us everything was going to be alright—and it was! Very professional and helpful—I can’t say enough about them all.”

— Carol • 5-star review on Avvo

“Someone I worked with recommended Sacks & Sacks. One of the best decisions of my life. Liz & Sherry went above & beyond in helping me with the bankruptcy. I will be forever grateful. I would highly recommend Sacks & Sacks to anyone.”

— Allen • 5-star review on Avvo

“They were great, very communicative and kept me up to date on everything going on. Would highly recommend.”

— Michele • 5-star review on Avvo

Read all 49 reviews on Avvo (4.8 rating) → • Google Reviews →

Stop paying fees on debt programs that aren’t working.

Call me for a free consultation. I’ll review your situation and tell you whether bankruptcy or consolidation is right for you. No judgment, no pressure — just honest answers from someone who’s done this over 6,000 times.

Frequently Asked Questions About Debt Consolidation in Jacksonville

Is debt consolidation the same as bankruptcy?

No. Debt consolidation combines multiple debts into one payment, usually through a new loan or management plan — you still repay what you owe. Bankruptcy is a federal court process that either discharges qualifying debts entirely (Chapter 7) or restructures them into a court-supervised repayment plan (Chapter 13). Consolidation is voluntary for creditors; bankruptcy is court-ordered.

Will debt consolidation hurt my credit score?

It can. If the consolidation company advises you to stop making payments while they negotiate, those missed payments will appear on your credit report. Settlement notations also lower your score. While bankruptcy does appear on your credit report for 7-10 years, many filers see their scores recover by 100-150 points within the first year after discharge. [4]

How much does debt consolidation cost in Florida?

Fees vary widely. Debt settlement companies typically charge 15-25% of your enrolled debt. For example, if you enroll $50,000 in debt, you may pay $7,500-$12,500 in fees alone — before any debt is actually settled. Nonprofit credit counseling agencies charge lower fees but cannot negotiate debt reductions. By comparison, Chapter 7 bankruptcy filing fees are approximately $338, plus attorney fees.

Can I file bankruptcy if I already started a debt consolidation program?

Yes — and in my experience, many clients come to me after consolidation failed. You can file for bankruptcy at any time, even if you are enrolled in a consolidation program. If you have been making payments to a consolidation company, those payments are generally not recoverable, which is why I always recommend evaluating all your options before committing to any program. The sooner we talk, the more options you have.

What debts can bankruptcy discharge that consolidation cannot?

Chapter 7 bankruptcy can completely eliminate credit card debt, medical bills, personal loans, utility arrears, and certain other unsecured debts. Consolidation does not eliminate any debt — it only restructures the payment terms. Additionally, bankruptcy’s automatic stay stops wage garnishments, lawsuits, and creditor calls immediately upon filing, which consolidation cannot do.

How long does it take to recover financially after bankruptcy vs. consolidation?

Chapter 7 bankruptcy resolves debts approximately 40% faster than consolidation programs. [6] Most Chapter 7 cases complete within 3-4 months. Consolidation programs typically take 3-5 years and have a 32% dropout rate. After bankruptcy discharge, 50% of filers secure new credit within 12-18 months. And every client at Sacks & Sacks gets my 7 Steps to a 720 Credit Score program to accelerate that recovery.

Serving Jacksonville, Orange Park, St. Augustine, Fernandina Beach, and all of Northeast Florida. Virtual consultations available — no office visit required.

Related: Jacksonville Bankruptcy Lawyer | Chapter 7 Bankruptcy | Chapter 13 Bankruptcy | Personal Bankruptcy | Business Bankruptcy | Fast File Bankruptcy | 7 Steps to a 720 Credit Score

Sources

[1] Hoyes Michalos study, as cited by Bowin Law, 2025. 80% of debt consolidation applicants fail to qualify. 32% dropout rate from DebtWave 2024 study.

[2] Nolo. (2025). America’s Bankruptcy Comeback: Why 2025 Bankruptcy Filings Are Surging. https://www.nolo.com/news/. Total filings: 542,529 (+11.8%). Credit card debt: $1.21 trillion.

[3] Debt.org. (2025). Bankruptcy filings statistics, calendar year 2024. Florida: 37,156 filings. National: 517,308 (+14.2% from 2023).

[4] Experian. (2024). Credit score recovery data showing 100-150 point improvement within 6-12 months of Chapter 7 discharge.

[5] Upsolve tracking data and FindLaw. 70% of Chapter 7 filers report improved stability within 3 years. 50% secure new credit within 12-18 months.

[6] Guardian Litigation. (2024). Chapter 7 resolves debts approximately 40% faster than consolidation programs.