Doubled since 1990

The divorce rate for Americans ages 50 and older has roughly doubled since 1990, and tripled for those 65 and older. Gray divorce is now one of the fastest-growing family-law trends in the country, and Florida law has shifted hard beneath it.

Gray divorce, the legal end of a marriage when at least one spouse is 50 or older, is no longer a rare outlier. It is a structural shift in American family life. In 1990, the idea of splitting at 60 or 70 still carried stigma and, for many women, a near-total loss of financial footing. By 2026, it is mainstream enough to have its own peer-reviewed literature, its own financial-planning subspecialty, and, in Florida, an entire legislative reform aimed squarely at it.

This article pulls together the most current data on how common gray divorce has become, who files, what it costs financially, and how Florida law treats a late-life split after the 2023 alimony overhaul. Every statistic below links to its source. Where an older figure has been widely repeated online but does not hold up against the original research, I have flagged the correction.

A gray divorce is the legal dissolution of a marriage in which at least one spouse is age 50 or older at the time of filing. The label comes from the 2004 AARP Divorce Experience study and was cemented in academic use by Susan Brown and I-Fen Lin at Bowling Green State University’s National Center for Family and Marriage Research (NCFMR). Today it is the working term used by Pew, the U.S. Census Bureau, the APA, and essentially every family-law bar in the country.

Across the research literature, the cutoff is a clean 50. Some older studies used 55 or 60, which is why certain legacy statistics will not line up cleanly, but the current norm in Pew, NCFMR, and Journals of Gerontology publications is age 50 at the time of filing. [1]

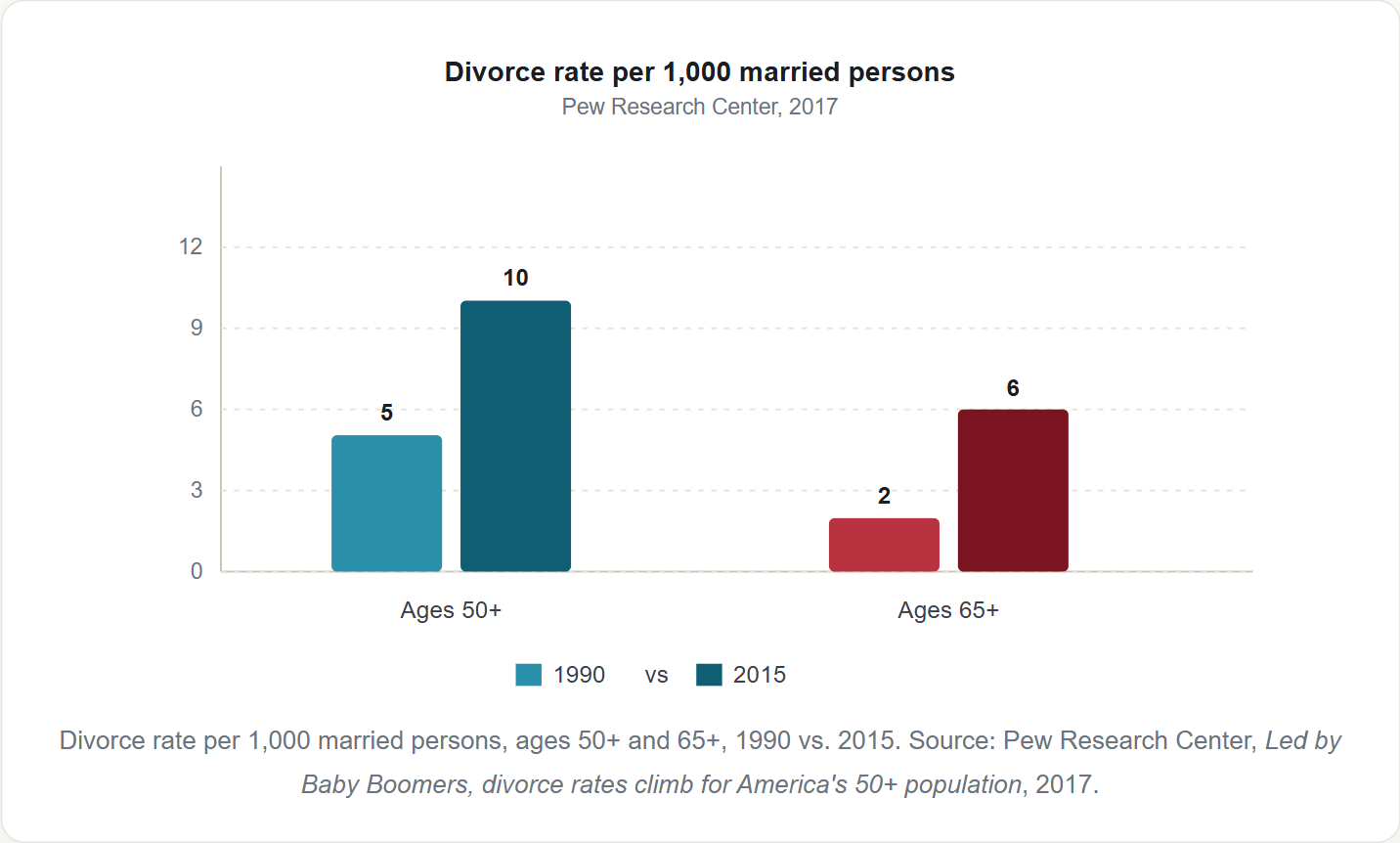

The single clearest statistic in this field: for every 1,000 married Americans ages 50 and older, 10 divorced in 2015, up from 5 in 1990. [2] For adults 65 and older, the rate tripled over the same period, from 2 per 1,000 to 6 per 1,000.

That doubling matters because the overall U.S. divorce rate has been drifting down since the early 1980s. Divorce is becoming less common for everyone except people over 50, where it is surging.

From the Practice:

In my Jacksonville office, the age profile of the intake calendar has flipped over the last decade. Twenty years ago, most first consultations were with clients in their 30s and early 40s. Today, roughly a third of my consultations are with spouses over 55, often after a 25- or 30-year marriage. The conversation is almost never about misconduct. It is about compatibility, a retirement horizon, and what the next 20 years should look like.

Among all U.S. divorces in a given year, roughly one in four involves at least one spouse age 50 or older. That share has grown steadily from about 1 in 10 in 1990 (Pew Research, 2017). [2] NCFMR’s more recent analyses put the 50+ share closer to 36% in the 2020s for filings involving spouses 55 and older, although methodologies vary slightly.

Two forces drive the increase. First, Boomers are simply a large cohort now aging into this bracket. Second, and more important, their per-capita divorce rate is rising, not just their absolute count. Earlier generations stayed married longer at the same age.

The U.S. Census Bureau reports that the percentage of Americans who have ever been divorced peaks at about 43% for ages 55 to 64, the highest share of any age group. [3]

That lifetime number matters for a different reason: it means nearly half of Americans at retirement age are walking into their 60s with a prior divorce in their history, often with a remarriage, blended children, and multiple retirement accounts titled in different ways. Second-marriage dissolutions are a big share of the gray-divorce caseload, and the financial planning is usually harder than a first-marriage split.

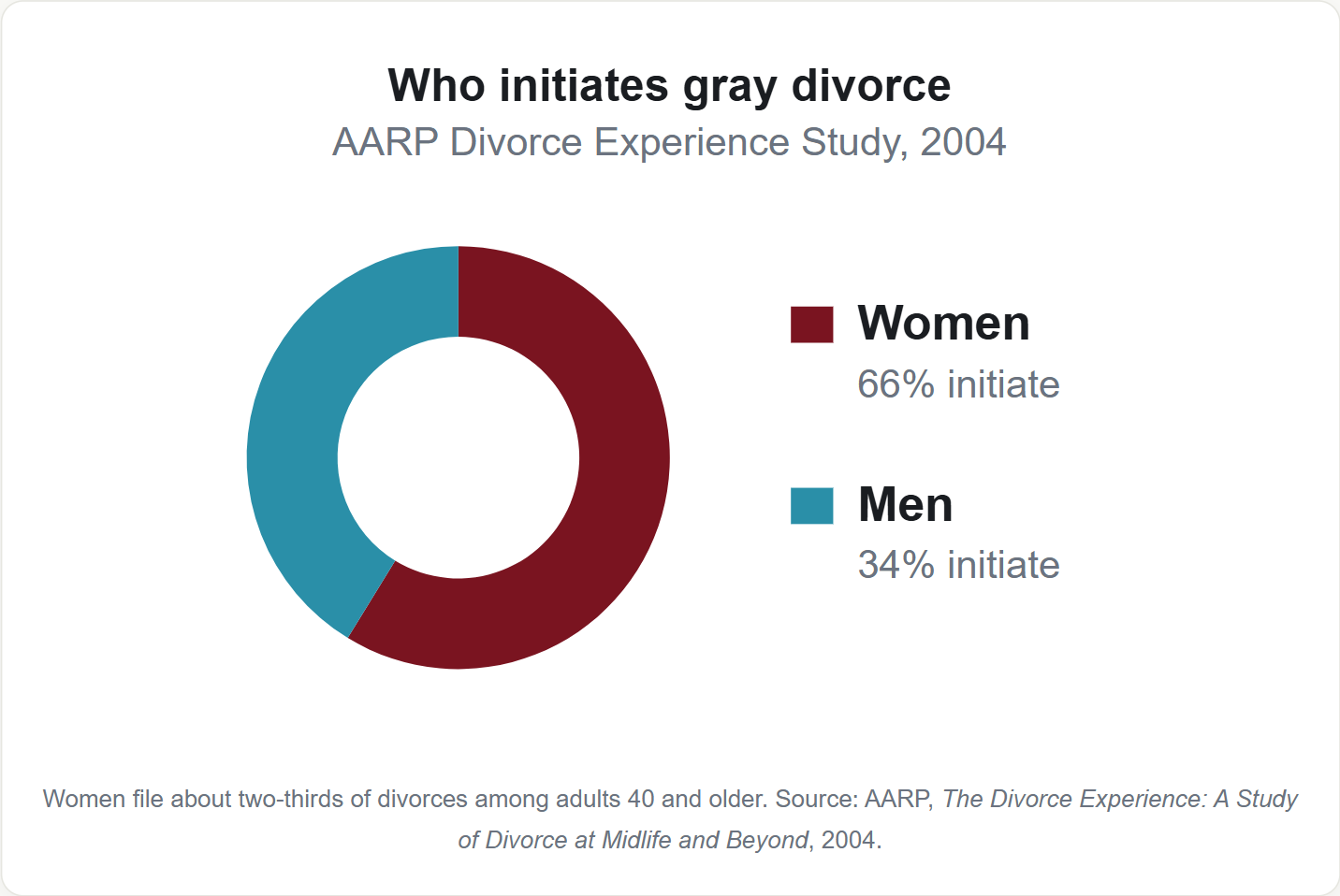

The best-sourced figure on who files is 66%, drawn from the 2004 AARP Divorce Experience study [4] of adults 40 to 79. More recent NCFMR work suggests the share has held steady into the 2020s, with women initiating about two-thirds of divorces at midlife and later.

The usual explanation is that many long marriages reach the empty-nest transition with the two spouses on very different life plans, and women are no longer as financially trapped as they were in their mothers’ generation. That change, dual-earner careers, women’s own retirement accounts, and longer female life expectancy, has changed the calculus of whether to stay.

The most important financial finding from the Lin and Brown (2021) analysis of the Health and Retirement Study: men and women both see about a 50% drop in household wealth after a gray divorce. [1] Pre-divorce mean assets of about $140,000 fall to roughly $66,000 for women and $59,000 for men. It is not a slow erosion; it is a one-time structural loss driven by splitting a single household into two.

After a gray divorce, women’s mean assets fell from $140,327 to $65,991, and men’s fell from $138,168 to $58,826, in both cases roughly a 50% drop relative to comparable still-married peers. [1]

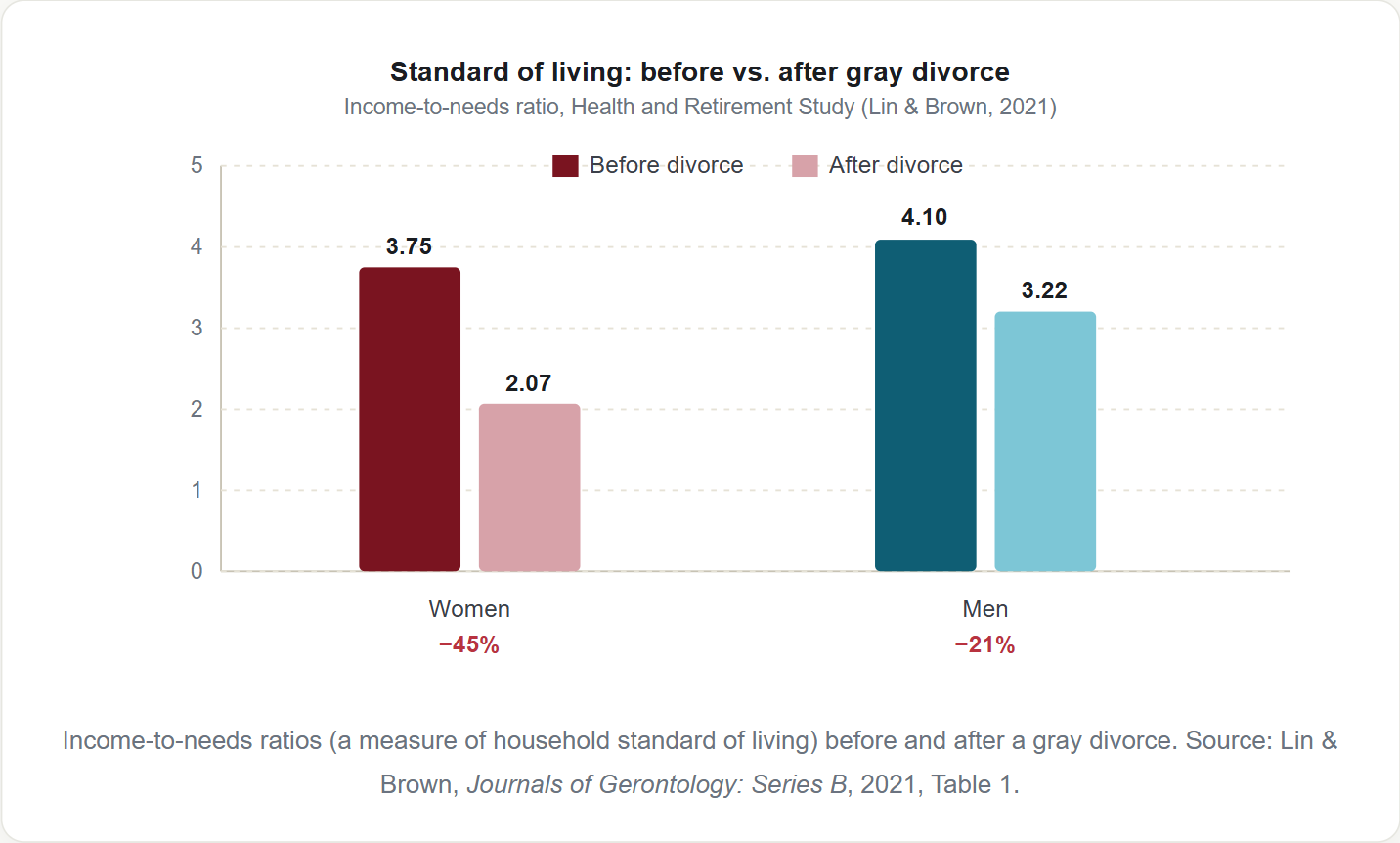

The more painful number, and the one earlier versions of this article got wrong, is standard of living. Using income-to-needs ratios from the Health and Retirement Study, Lin and Brown found that after a gray divorce, women’s standard of living falls 45% while men’s falls 21%. [1]

Three structural reasons for the gender gap: women in the 50+ cohort have lower lifetime earnings on average, lower Social Security benefits at their own work records, and often a longer gap out of the paid workforce for caregiving. Equitable distribution of marital assets does not fully correct for those underlying income streams, which is why post-divorce financial planning for a woman in her late 50s often needs a different playbook than for her ex-husband.

The academic literature points to four drivers. None are new, but they have compounded.

From the Practice:

When I ask long-married clients what tipped them, almost no one says “an affair” or “we stopped loving each other.” The most common answer is some version of “we looked at the next 20 years and could not agree on what they should look like.” Where one spouse wants to move near the grandkids and the other wants to travel, or one wants to retire at 62 and the other at 70, the gap is real, and it does not usually close.

Florida’s family-law framework has tightened around gray divorce in the last three years. If you are contemplating a split at 55 or older, these are the five legal levers that move the most money.

Florida is an equitable-distribution state under Fla. Stat. § 61.075. [6] Any retirement assets, 401(k)s, pensions, IRAs, deferred compensation, earned during the marriage are marital property and are divided equitably, which for long marriages usually means roughly 50/50. Splitting a qualified plan (a 401(k) or pension) requires a Qualified Domestic Relations Order (QDRO) drafted and approved after the final judgment. IRAs transfer via direct rollover without a QDRO.

Florida eliminated permanent alimony with SB 1416. [7] For gray divorces involving long marriages (20+ years) the available remedies are now:

The elimination of permanent alimony is the single biggest legal change for gray divorcing couples in Florida in 30 years. A 58-year-old spouse who did not work outside the home during a 30-year marriage can no longer count on support for the rest of her life. The planning implications, particularly for Social Security coordination and health insurance, are significant.

If a marriage lasted at least 10 years and the lower-earning ex-spouse is unmarried and at least 62, that ex-spouse can claim Social Security divorced-spouse benefits on the higher earner’s record, up to 50% of the higher earner’s full retirement amount (Social Security Administration). [5] This claim does not reduce the higher earner’s benefit and does not require their consent. Many gray divorce settlements miss this optimization entirely.

Florida’s homestead protections under Article X, § 4 of the state constitution complicate the sale of the marital home in a divorce. If the residence is homestead and there are no minor children, the spouses can generally sell or buy one another out with a stipulated judgment. Where one spouse wants to stay, the buyout math has to account for the homestead tax cap, property insurance changes, and the remaining mortgage, all of which can move $50,000 to $200,000 on a Jacksonville property.

Losing a spouse’s employer health plan at 55 is expensive. COBRA coverage runs 18 to 36 months but costs full premium plus a 2% administrative fee. ACA marketplace subsidies depend on post-divorce adjusted gross income, which for the lower-earner usually resets significantly. Medicare does not start until 65. Covering that gap is one of the first financial questions a gray divorce plan has to answer.

For a 30-year marriage in Florida, SB 1416 changed the alimony picture as follows.

| Remedy | Before July 1, 2023 | After July 1, 2023 (SB 1416) |

|---|---|---|

| Permanent alimony | Available for marriages 17+ years | Eliminated |

| Durational alimony | Up to length of marriage | Capped at 75% of marriage length (max 22.5 years on a 30-year marriage) |

| Bridge-the-gap | Up to 2 years | Up to 2 years (unchanged) |

| Rehabilitative | No hard cap | Capped at 5 years, requires written plan |

| Modification for retirement | Discretionary | Presumption in favor of modification at reasonable retirement age |

Three patterns from Jacksonville cases that do not show up in the national data:

The retirement-timing fight: The hardest part of a gray divorce is almost never custody. It is the question of when each spouse intends to retire, because durational alimony under SB 1416 can be modified at a “reasonable retirement age.” Whether that is 62, 65, or 67 is a negotiated term, and it can move $300,000+ in lifetime value.

Hidden pension value: Defined-benefit pensions, municipal, state, federal, military, are routinely undervalued in settlement because the parties focus on the account balances they can see on a statement. An actuarial present-value calculation on a 30-year pension often returns a number two or three times what the spouses assumed.

The second-marriage problem: For remarried gray divorcees, competing interests between a current spouse and adult children from a prior marriage create most of the heat. The estate plan, the beneficiary designations on retirement accounts, and the marital-home title all need to be rewritten before the judgment, not after.

Q. What is considered a gray divorce?

A gray divorce is the legal dissolution of a marriage in which at least one spouse is age 50 or older. The term entered mainstream use after the 2004 AARP study of midlife divorce and is now the standard label in academic and legal research for divorce at age 50+.

Q. Why are gray divorces increasing?

The divorce rate among adults 50+ has roughly doubled since 1990 (Pew Research, 2017). Longer life expectancy, declining stigma, women’s financial independence, and empty-nest transitions are the four drivers most often cited in peer-reviewed research, including Lin and Brown’s work at Bowling Green’s National Center for Family and Marriage Research.

Q. Who typically files for a gray divorce?

Women initiate roughly two-thirds of divorces at midlife and later. The 2004 AARP Divorce Experience study, still the most-cited source on this question, found women filed 66% of the time among adults 40 to 79. More recent NCFMR research shows the pattern has held into the 2020s.

Q. How is retirement savings divided in a gray divorce in Florida?

Florida is an equitable-distribution state (Fla. Stat. § 61.075). Retirement assets earned during the marriage, 401(k)s, pensions, IRAs, are marital property and split equitably, which usually means roughly 50/50 for long marriages. Splitting qualified plans requires a Qualified Domestic Relations Order (QDRO) drafted after the final judgment.

Q. How does gray divorce affect Social Security benefits?

If a marriage lasted at least 10 years and the lower-earning ex-spouse is unmarried and at least 62, that ex-spouse can claim Social Security divorced-spouse benefits on the higher earner’s record, up to 50% of the higher earner’s full retirement amount. This does not reduce the other spouse’s benefit and does not require consent.

Q. Is alimony paid in a Florida gray divorce after SB 1416?

Yes, but permanent alimony was eliminated effective July 1, 2023. Under SB 1416, long marriages (20+ years) are now eligible only for durational alimony capped at 75% of the length of the marriage, bridge-the-gap, or rehabilitative alimony. For a 30-year marriage, that means a maximum of 22.5 years of alimony instead of lifetime support.

Q. What is the average cost of a gray divorce in Florida?

Uncontested gray divorces typically run $1,500 to $5,000 in combined fees. Contested cases involving retirement accounts, a marital home, alimony, or a business routinely run $15,000 to $50,000+ per side. The biggest cost driver in gray divorces is valuation of retirement assets and pensions rather than custody.

Q. How long does a gray divorce take in Florida?

An uncontested Florida divorce generally finalizes in 4 to 8 weeks after the mandatory 20-day waiting period. Contested gray divorces average 9 to 18 months in Duval and surrounding counties, primarily due to financial discovery, valuation of retirement accounts, and, where needed, QDRO preparation after the final judgment.

Sources:

[1] Lin, I-F., & Brown, S. L. (2021). The Economic Consequences of Gray Divorce for Women and Men. Journals of Gerontology: Series B, 76(10), 2073–2085. pmc.ncbi.nlm.nih.gov/articles/PMC8599059

[2] Pew Research Center. (2017, March 9). Led by Baby Boomers, divorce rates climb for America’s 50+ population. pewresearch.org

[3] U.S. Census Bureau. (2021, April 22). Number, Timing and Duration of Marriages and Divorces: 2016. census.gov

[4] AARP. (2004). The Divorce Experience: A Study of Divorce at Midlife and Beyond. aarp.org

[5] Social Security Administration. Benefits for a divorced spouse. ssa.gov

[6] Florida Statutes § 61.075 (Equitable distribution of marital assets). leg.state.fl.us

[7] Florida Senate Bill 1416 (2023). Dissolution of Marriage. flsenate.gov

[8] Bowling Green State University, National Center for Family and Marriage Research (NCFMR). bgsu.edu/ncfmr

[9] American Psychological Association. (2023, November 1). More couples are divorcing after age 50 than ever before. apa.org/monitor

[10] Upham, B. (2023, June 2). ‘Gray Divorce’ Is on the Rise. Everyday Health. everydayhealth.com

Reviewed by

Family Law Attorney & Partner, Sacks & Sacks